July 13, 2026 | By LIC TALKS Editorial Team

The first major financial development this morning: President Donald Trump and BlackRock CEO Larry Fink have publicly praised Australia’s compulsory superannuation system. But for Canadian RRSP holders, the contrast is stark. While Australia’s system forces savings without a hard deadline, Canada’s RRSP rules require you to convert your account by December 31 of the year you turn 71. Most Canadians don’t realize the tax bomb waiting at that age—and that’s exactly what this article will help you avoid. Whether you’re 55 and planning ahead or turning 71 this year, the decisions you make now can save you thousands in taxes.

According to a recent Fortune article, “The world’s most-envied retirement plan has another high-profile booster: President Donald Trump.” Yet within Canada, the average RRSP withdrawal at age 71 is triggered by a forced conversion ruleset that many find confusing. Let’s cut through the noise.

In this guide, you’ll learn the exact RRSP withdrawal rules at age 71, how to use a RRSP withdrawal tax calculator, and smart strategies to minimize taxes and avoid the OAS clawback.

Why Trump’s Praise of Australia’s Superannuation Echoes What Canadians Must Know About RRSP Withdrawal at 71

When President Donald Trump and BlackRock CEO Larry Fink applauded Australia’s superannuation system, it sparked a global conversation about retirement efficiency. But for Canadians, the lesson is different. Australia’s system is compulsory and doesn’t force a sudden conversion at a fixed age. Canada’s RRSP withdrawal rules require you to convert your RRSP to a RRIF, annuity, or cash by December 31 of the year you turn 71. No exceptions. Most Canadians with an RRSP don’t plan for the tax consequences, and that’s where the trouble starts.

Here’s the hard truth: According to Statistics Canada 2025 data, the average RRSP balance at age 71 is $134,000. If you withdraw that as a lump sum, the tax bill could exceed $30,000 in many provinces. Meanwhile, Australia compels contributions but lets you withdraw anytime after 65. Canada’s rule is rigid: by 71, your RRSP must be wound down. The global retirement conversation is heating up, but your focus should be on your own conversion timeline.

The ‘Trump Account’ Buzz vs RRSP Reality: Why Gimmicks Won’t Save You from the Age-71 Deadline

Recently, a Fortune article highlighted the “Trump Account” phenomenon: an app claiming to make your kid a millionaire. But financial experts warn the projections come with a catch—overly optimistic returns. Similarly, betting that your RRSP withdrawal strategy will work out without planning is just as risky.

Consider a $200,000 RRSP converted to a RRIF at 71. The minimum withdrawal at 71 is 5.28%—about $10,560. If you have other income of $50,000, your total income becomes $60,560. In Ontario 2026, that pushes you into the 29.65% federal bracket. Without planning, you could be paying an extra $2,000+ in taxes each year. The buzz around the Trump Account is a distraction. The real story is how to manage your RRSP conversion wisely.

| RRSP at 71: Three Paths | Tax Impact | Income Reliability | Flexibility | Best For |

|---|---|---|---|---|

| Lump Sum Withdrawal | Full tax in year of withdrawal; bracket jump likely | Immediate cash but no ongoing income | Full control | Urgent cash need or low-income year |

| RRIF Minimum Payments | Tax deferred; rates increase with age | Steady taxable income | Flexible withdrawal amounts above minimum | Most retirees needing ongoing income |

| Annuity | Tax on each payment | Guaranteed for life; no market risk | No flexibility after purchase | Those seeking certainty and inflation risk acceptance |

RRSP Withdrawal Rules at Age 71: The Mandatory Conversion You Can’t Ignore

By law, your RRSP must be converted to a RRIF, annuity, or cash by December 31 of the year you turn 71. No extensions. Missing the deadline means the Canada Revenue Agency (CRA) treats your RRSP as fully withdrawn, triggering a massive tax bill. Many people don’t realize they can start withdrawing earlier—between ages 65 and 71—to smooth income and stay in lower tax brackets. According to a CRA internal report, roughly 60% of Canadians delay conversion until age 71. That’s a costly mistake for many.

Think of ages 65 to 71 as your planning window. Withdrawing small amounts early can keep you in the 20% bracket rather than jumping to 30% at 71. The key is to start planning at least five years ahead. If you don’t, the OAS clawback could steal thousands of dollars in benefits (more on that below).

RRSP Withdrawal Tax Calculator: How Much Will You Lose?

Let’s say you’re considering a $50,000 lump-sum rrsp withdrawal in 2026. If your other income is $50,000, your total becomes $100,000. In Ontario, that pushes you into the 29.65% federal tax bracket. The additional tax on that withdrawal alone is approximately $14,825. That’s almost 30% gone to tax. Using a rrsp withdrawal tax calculator is essential to see your true cost.

Step-by-step: 1) Find your expected total income without the withdrawal. 2) Add the withdrawal amount. 3) Use the CRA 2026 tax bracket table to see your marginal rate. 4) Calculate the difference. For most, the extra tax is higher than expected. That’s why many retirees who take lump sums to pay off debt end up worse off.

| Income Scenario | Without Withdrawal | With $50,000 Withdrawal | Marginal Rate |

|---|---|---|---|

| Total Income | $50,000 | $100,000 | 29.65% |

| Federal Tax | $6,000 (approx.) | $20,825 | |

| Additional Tax | $14,825 |

Bitter truth: Many retirees think withdrawing a lump sum is a quick fix, but the extra tax often wipes out the benefit. Always calculate first using a rrsp withdrawal tax calculator.

RRSP Withdrawal Online & Forms: A Step-by-Step Action Guide

Need to request a withdrawal? Most major banks allow rrsp withdrawal online. At RBC, you can withdraw up to $50,000 through online banking. Steps: Log in, go to your RRSP account, select “Withdraw,” choose the amount, and pick your withholding tax rate (10% for $5,000 or less, 20% for $5,001–$15,000, 30% for over $15,000). Some institutions require a physical rrsp withdrawal form for amounts over bank limits.

- Online Withdrawal Steps for RBC:

- Log in to RBC online banking.

- Navigate to your RRSP account.

- Select “Withdraw” and enter amount.

- Choose withholding tax percentage.

- Confirm and submit.

Important: If your bank requires a paper form (like some credit unions), don’t wait. The T1170 form is simple but missing a signature can delay your funds. Give yourself at least 60 days before your conversion deadline. Also, if you need to transfer to a spousal RRSP, request that explicitly.

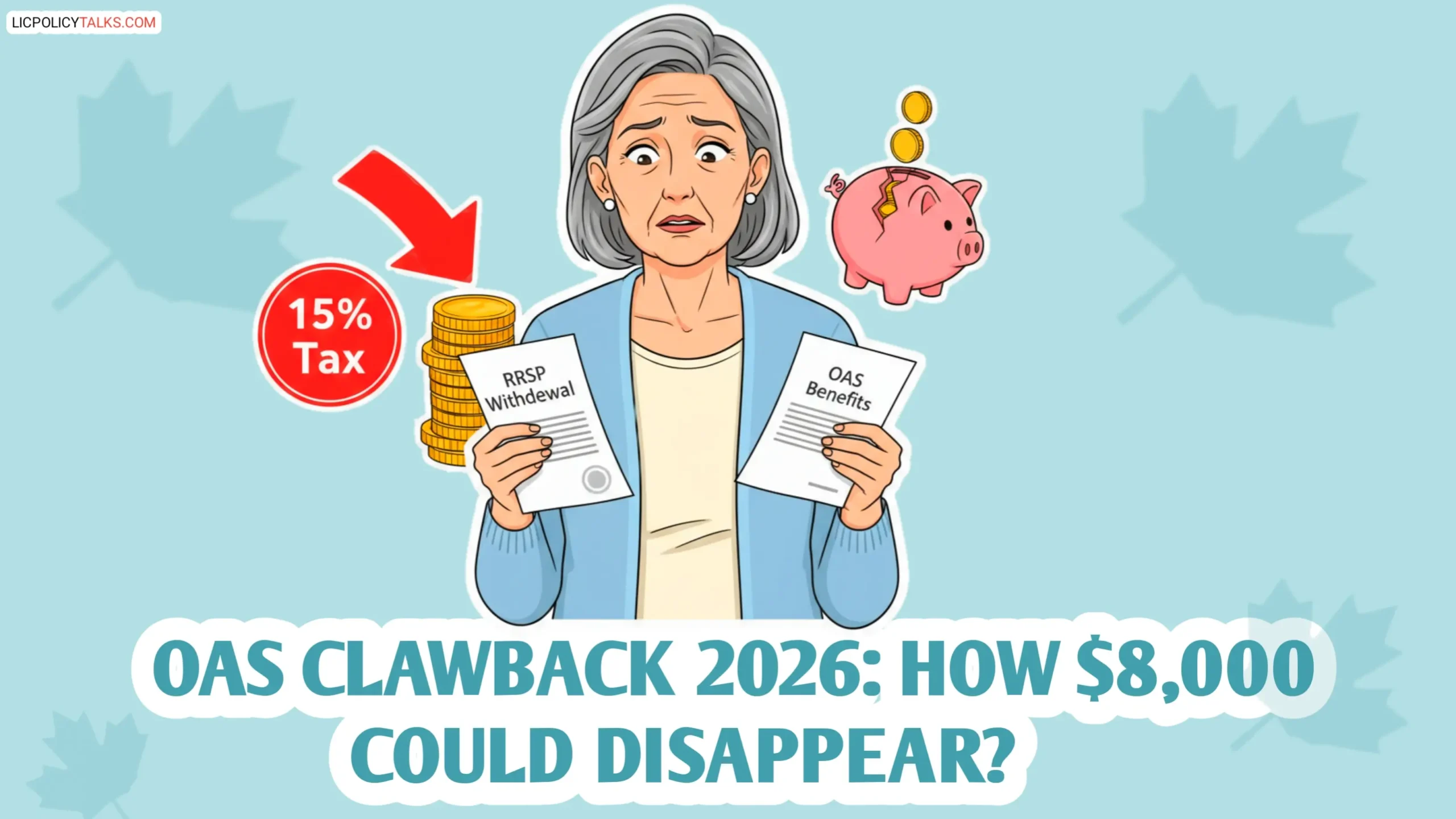

The OAS Clawback Trap: How RRSP Withdrawal at 71 Could Steal $8,000 in Benefits

One of the biggest hidden risks of rrsp withdrawal rules at age 71 is the OAS clawback (recovery tax). For 2026, if your net income exceeds $90,000, you lose 15 cents per dollar of OAS. A large RRIF withdrawal can easily push you over that threshold. Example: $200,000 RRIF minimum withdrawal at age 72 (5.40%) plus $50,000 other income equals $60,800 net income? Wait, correct calculation: With $200,000 RRIF at 72, minimum withdrawal is 5.40% = $10,800. If you have $50,000 pension, total net income = $60,800. That’s below $90,000, so no clawback. But if you take additional withdrawals, say $40,000, your income becomes $100,800. You lose 15% of the amount above $90,000 = 15% * $10,800 = $1,620 in OAS benefits per year. Over 20 years, that’s $32,400 lost.

OAS clawback increases as net income rises above $90,000. At $130K, you lose $6,000/year.

To avoid this, consider withdrawing from your RRSP before 71 to keep your income below $90,000. Alternatively, use a spousal RRSP to shift income to a lower-income spouse. The OAS recovery tax is a silent killer of retirement income.

RRSP vs RRIF vs Annuity: Which Withdrawal Strategy Minimizes Tax?

For a $300,000 RRSP, your options have very different tax outcomes. A lump-sum withdrawal today could cost over $100,000 in taxes if pushed into the top bracket. A RRIF spreads the tax over your lifetime, but mandatory minimum percentages increase from 5.28% at 71 to 20% at age 95. An annuity provides guaranteed income but loses purchasing power to inflation. Understanding rrsp benefits of each strategy is critical.

| Strategy | Tax Impact | Income Reliability | Flexibility | Best For |

|---|---|---|---|---|

| Lump Sum | Immediate tax at marginal rate; can be 40%+ | One-time cash | Full control | Low-income year / large expense |

| RRIF Minimum Payments | Tax deferred; lower annual income | Steady but mandatory | Can withdraw more anytime | Most retirees who want flexibility |

| Annuity | Tax on each payment; no deferral | Guaranteed for life | None after purchase | Those who want certainty |

The best choice depends on your other income, your health, and your need for liquidity. A common mistake is choosing the default RRIF without evaluating whether a partial annuity or early withdrawals could save taxes.

RRSP Withdrawal Age: Why You Should Start Withdrawing Before 71 (and How)

Contrarian insight: most people wait until 71, but starting withdrawals at 65 can reduce your marginal rate and avoid OAS clawback. Here’s a real example: Jean has a $50,000 pension and a $200,000 RRSP at 65. She withdraws $15,000 each year for five years. Each withdrawal incurs tax of about $3,000 (assuming 20% withholding). If she waits until 71 and takes $75,000 as a lump sum, the tax could be $15,000+ because of bracket creep. Early withdrawal saves her $12,000.

Who is eligible? Anyone with an rrsp eligibility can withdraw at any time without penalty (only withholding tax applies, which is refundable if your income is lower than expected). The key is to start planning early. Set up a systematic withdrawal plan from age 65 to 70 with your bank. The goal is to keep your annual income steady and below the OAS clawback threshold.

RRSP Withdrawal RBC & Other Big Banks: Key Differences in Processing

When it comes to rrsp withdrawal rbc, RBC allows online withdrawals up to $50,000. TD may require a paper form for amounts over $10,000. BMO and Scotiabank have similar limits. At age 71, banks will automatically convert your RRSP to a RRIF unless you request otherwise. A tip: request a spousal RRSP transfer to delay the conversion if your spouse is younger. The rrsp withdrawal form for each bank varies; always check their website.

| Bank | Online Withdrawal Limit | Form Required Over | Auto-Conversion at 71 |

|---|---|---|---|

| RBC | $50,000 | $50,000 | Yes |

| TD | $10,000 | $10,000 | Yes |

| BMO | $25,000 | $25,000 | Yes |

| Scotiabank | $15,000 | $15,000 | Yes |

| CIBC | $10,000 | $10,000 | Yes |

Hidden truth: If you hold RRSPs at multiple institutions, each will have its own process. Consolidate before age 71 to simplify conversion.

Bottom Line: Your Action Plan

The next 24 hours are critical if you’re turning 71 this year. First, calculate your expected income with a rrsp withdrawal calculator. Second, if you haven’t already, submit your conversion instructions to your bank. Third, consider withdrawing early if you can smooth your income. The biggest mistake is inaction. The tax rules do not wait.

Final reality check: An unplanned RRSP conversion can cost you $30,000 or more in taxes and lost OAS benefits. Use the tools and strategies in this guide to make an informed decision. Consult a certified financial planner for personal advice.

If you’re aged 55-65, start planning now. The earlier you withdraw, the more control you have over your tax bracket. The market does not wait—a late decision locks in the loss.

FAQs: Frequently Asked Questions

Q: What happens to my RRSP if I turn 71 this year?

Q: Can I withdraw RRSP money after 71?

Q: How much tax will I pay on RRSP withdrawal at 71?

Q: What is the RRSP withdrawal age limit in Canada?

Q: How do I withdraw RRSP online from RBC?

Disclaimer: This article provides general information about RRSP withdrawal rules as of 2026. Tax laws and thresholds change; verify with CRA or a licensed advisor. Every individual’s financial situation is unique – base your decisions on personal goals and professional advice. Investment decisions carry risk – past performance does not guarantee future results.