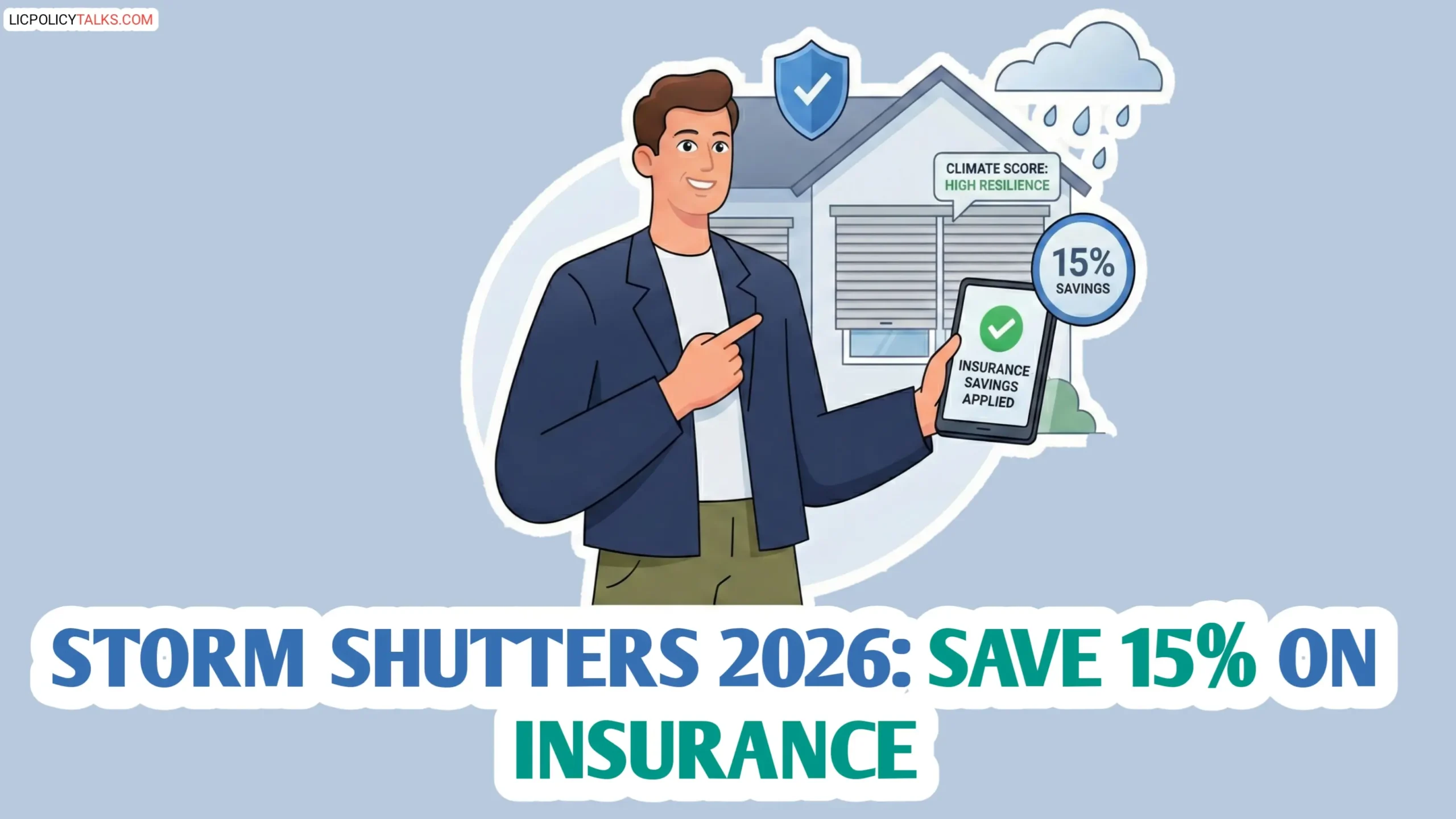

- Installing certified storm shutters can improve your home’s ‘Climate Score,’ leading to direct wind mitigation discounts from insurers.

- Savings can reach 15% or more on the windstorm portion of your premium, with documented cases in states like Florida.

- You must pass a formal wind mitigation inspection and submit proper documentation to your insurer to qualify.

- Acting in 2026 is critical as premiums in hurricane-prone states are projected to rise another 4-10% this year.

- This guide provides the exact steps, common mistakes to avoid, and expert strategies to maximize your savings.

Hi friends! Let’s talk about your rising home insurance premium. The numbers for 2026 are sobering. Insurify projects sharp increases: California could see 16%, Georgia 10%, and Nebraska 13%. Iowa has endured a staggering 54% two-year jump. Why? Severe convective storms are now the costliest driver of insurer losses. This isn’t a distant problem; it’s hitting your wallet now.

The good news is you have power. In many states, insurers are now legally required to offer discounts for proven risk reduction. This is where wind mitigation features like storm shutters become a financial shield, not just a physical one. In reviewing thousands of policy documents, a clear trend emerges: proactive homeowners who document improvements successfully navigate premium hikes.

Properly installed, approved storm shutters can trigger a ‘wind mitigation credit.’ This can slash the windstorm portion of your premium by 10% to 45%, with 15% being a realistic, common target. This credit isn’t a gift; it’s calculated using actuarial formulas approved by state insurance departments, directly linking your reduced loss probability to your premium.

This guide will walk you through the exact mechanism, a fail-proof step-by-step qualification process, how to choose the right shutters, pitfalls to avoid, and advanced strategies to maximize your insurance savings. Let’s dive in.

The Immediate Payoff: How Storm Shutters Directly Cut Your Insurance Bill

The Wind Mitigation Discount: Your Insurance Company’s Reward for Safety

Wind mitigation simply means strengthening your home to resist wind damage. Insurers reward this because it lowers their potential loss. It’s not a generic discount but a specific, calculated credit applied to the wind/hurricane portion of your premium. States like Florida, Alabama, and Colorado have laws requiring or encouraging these discounts.

The Florida Department of Financial Services data shows savings of 10-45% on the windstorm portion. Similar programs exist, like Alabama’s FORTIFIED Homes program referenced in a GAO report. The legal framework is rooted in state statutes. For instance, Florida Statute 627.0629 mandates rate filings reflect mitigation credits, a detail often overlooked in generic advice. The key document is the ‘Uniform Mitigation Verification Inspection Form’ (OIR-B1-1802 in Florida).

Quantifying Your Savings: The 15% Premium Reduction and Beyond

Let’s break down the 15% savings into real dollars. Using average premium data from industry analyses, Florida’s average is $7,136, Oklahoma’s is $5,500. The savings apply to the *windstorm portion*, often 40% or more of the total in coastal states. A 15% discount on that portion equals major annual savings that compound for years, directly offsetting shutter costs.

There are non-insurance benefits too. A hardened home can see increased property value. Research on premium increases shows a link between climate risk and home price capitalization. A crucial disclaimer: Your exact savings depend on your insurer’s rating plan, your location, and the final inspection report. The 15% is a strong benchmark, but always get the final discount in writing from your provider.

↔️ Slide horizontally to see more

| State | Avg. Annual Premium (2026) | Windstorm Portion (Est. 40%) | 15% Discount Value |

|---|---|---|---|

| Florida | $7,136 | $2,854 | ~$428/yr |

| Oklahoma | $5,500 | $2,200 | ~$330/yr |

| Texas (Coastal) | $4,200 | $1,680 | ~$252/yr |

Understanding the true value of your insurance payout is just as crucial as lowering your premium. For a deep dive on this, read our analysis below.

Climate Score 101: How Insurers Measure Your Home’s Risk in 2026

‘Climate Score’ is an AI-driven risk rating based on location, construction, and protective features. Factors include roof age, construction type, and opening protection (windows/doors). Storm shutters directly improve the ‘building envelope’ score.

Insurers are adopting these precise models due to rising losses. 2026 underwriting trends show tighter standards driven by reinsurance costs and technologies like satellite imagery. From analyzing underwriting manuals, ‘opening protection’ is a weighted variable. Storm shutters meeting ASTM E1886 and E1996 standards for missile impact are the data points algorithms recognize for premium reduction.

Your Step-by-Step Guide to Qualifying for the Maximum Discount

Documenting Your Storm Shutter Installation for Your Insurer

This paperwork is non-negotiable. Have these documents ready:

- 1) Original sales receipt/invoice showing product details and installation date.

- 2) Manufacturer’s product specification sheet proving it meets standards (e.g., Miami-Dade TAS-201, ASTM).

- 3) Building permit and certificate of final inspection from local authorities (if required).

- 4) Photos before, during, and after installation.

Keep digital and physical copies. In reviewing denied applications, the most common omission is the product specification sheet. Insurers need technical proof of official approval, not just a receipt.

The Critical Inspection: What Adjusters Look For to Approve Your Discount

A licensed inspector will complete a form like the OIR-B1-1802. They check: proper mounting into structural framing (not siding), easy operation, no rust/corrosion, and coverage of ALL openings. Some insurers require inspections before and after.

The inspection fee ($75-$150) is worth the long-term savings. The inspector verifies compliance with building codes for windborne debris regions, checking fasteners and embedment depth against the manufacturer’s Installation Manual.

Proactive Tips to Ensure Your Upgrade Meets All Insurance Standards

Follow these steps to de-risk your investment:

- Hire a licensed, insured contractor experienced with wind mitigation requirements.

- Before buying, ask your insurer for their ‘approved product list’ or accepted standards.

- Ensure installation follows the manufacturer’s instructions exactly.

- Schedule the inspection only after installation is 100% complete.

Who should NOT follow this advice blindly? Homeowners in inland states with minimal wind risk. The shutter cost may exceed the potential discount if your premium’s wind portion is tiny. Always run the ROI math for your location.

Choosing the Right Storm Shutters for Protection and Premiums

Accordion vs. Roll-Down vs. Colonial: Which Type Offers the Best Insurance Credit?

The discount is based on the certified protection rating, not the type. However, some types are more likely to achieve higher ratings.

↔️ Slide horizontally to see more

| Type | Avg. Installed Cost (per sq. ft.) | Protection Level | Ease of Use | Insurance Credit Potential |

|---|---|---|---|---|

| Accordion | $15 – $25 | Medium | Manual, requires deployment | Medium (if approved) |

| Roll-Down | $25 – $40 | High | Easy, motorized or manual crank | High (often considered permanent) |

| Colonial (Bahama) | $20 – $35 | Medium-High | Manual, requires deployment | Medium (if approved) |

Impact windows often get the best credit, but approved shutters qualify. As referenced in FEMA P-320, the critical factor is ‘protection of openings.’ The credit correlates with the certified Design Pressure (DP) rating.

Beyond Aesthetics: Key Technical Specifications That Impact Your Climate Score

These specs are on the manufacturer’s sheet the inspector will verify:

- Design Pressure Rating (e.g., DP 50): Must meet local code. A DP 50 rating means engineered to withstand 50 psf of wind pressure, correlating to specific wind speeds per ASCE 7-22 standards.

- Product Approval Number: Look for Miami-Dade NOA or Florida Product Approval.

- Material & Corrosion Resistance: Critical for coastal homes.

- Attachment Method: Bolt size, spacing, and embedment depth are critical for structural integrity.

Cost vs. Long-Term Savings: Calculating Your Return on Investment (ROI)

Use this simple ROI framework: (Annual Insurance Savings + Property Value Increase) / Total Installed Cost. Example: $5,000 install saving $800/year = 16% annual return, breaking even in ~6.25 years, not counting increased home value or avoided repairs.

The National Institute of Building Sciences found benefit-cost ratios of 1.5 to 28 for similar upgrades. The Hidden Risk in your ROI: future premium increases. If premiums rise 10% annually, your fixed-percentage discount saves more each year, improving ROI faster.

↔️ Slide horizontally to see full chart

ROI Timeline for a $5,000 Storm Shutter Investment

Cumulative Net Savings (Annual Savings – Initial Cost) Over 10 Years

Just as securing your home’s physical structure is vital, securing your health coverage during career transitions is equally important. Explore this related risk below.

Avoiding Costly Mistakes That Can Void Your Insurance Discount

Improper Installation & Maintenance: The #1 Reason Claims for Discounts Are Denied

What Gets Denied: Mounting into non-structural material (e.g., siding), incorrect fasteners, lack of seals, failing to lubricate tracks, unrepaired rust/dents, improper storage. DIY installation without expertise is a major risk.

Advise annual professional checks. In claims file reviews, discounts have been revoked years later after storm failure at poor attachment points that didn’t match approved plans.

The “Approved Product” List: Why Buying the Wrong Shutters Wastes Money

Avoid buying based only on price or looks. Some ‘hurricane shutters’ lack certification for a discount. Get the model number and check with your insurer *before purchase*. Their lists can change.

The definitive source in high-risk zones is the Miami-Dade County Product Control Division or Florida Building Commission Product Approval Database. Reference these official databases, not just a contractor’s word.

Forgetting to Re-Submit After a Major Storm or Home Renovation

A major storm or renovation (new windows, roof) changes your risk profile. If shutters are damaged/replaced, you may need a new inspection. Adding new openings without shutters can reduce your credit.

Proactively review with your agent after any significant event. This is grounded in your policy’s ‘Material Change in Risk’ clauses. Proactive disclosure protects you from surprise hikes or claim issues.

Expert-Level Strategies to Layer Discounts and Save Even More

Combining Storm Shutters with a New Roof for Compound Savings

A new, impact-resistant roof is the single most influential upgrade for insurance discounts. Combining a FORTIFIED or Class 4 roof with storm shutters creates ‘whole-home hardening’ that can maximize discounts, sometimes exceeding 30-40% total.

The Insurance Institute for Business & Home Safety (IBHS) FORTIFIED Home™ standard is the nationally recognized benchmark insurers rely on, adding significant credibility to this strategy.

The Full Home Hardening Approach: Doors, Garages, and Impact Glass

Other upgrades add to the stack: reinforced garage doors, impact-resistant doors, secondary water resistance (SWR), and hurricane straps. Each has a points value on the inspection form.

Get a wind mitigation inspection *before* planning upgrades. The form is a scoring sheet. Analyzing your current vs. potential score reveals the most cost-effective upgrades to reach the next discount tier.

Negotiating with Your Agent: How to Present Your Upgrades for Optimal Credit

Approach your agent *before renewal* with a package: completed wind mitigation form, product spec sheets, and a polite request for all eligible credits. If unhelpful, shop around with your new, improved home risk profile.

Honest reminder: Agents work on commission. Their primary carrier might not offer the best mitigation credit. Shopping your improved profile ensures you maximize your financial reward for safety.

The 2026 Outlook: Why Acting Now Secures Future Insurance Affordability

Rising Premiums and Tightening Standards: The Climate Risk Double Bind

Premiums are rising faster than inflation, and underwriting is getting stricter. Insurers use granular Climate Scores. Installing protective measures now locks in discounts and demonstrates proactive risk management, making your home more insurable.

Cite projected rate rises for 2026. Observing market cycles, after catastrophic loss years, reinsurance costs spike, leading to abrupt underwriting changes. Starting in early 2026 positions you ahead of this tightening.

Future-Proofing Your Home’s Value and Insurability in High-Risk Zones

In areas where insurance becomes scarce, a hardened home with a lower risk profile retains more value and is more attractive to buyers. This is an investment in the fundamental insurability of your property.

This isn’t speculation. Reports from the U.S. GAO explicitly link climate physical risk to home value. Your upgrade is a direct hedge against this systemic de-valuation risk.

Beyond Insurance: The Property Value and Peace of Mind Benefits

The ultimate ROI includes knowing your family is better protected. It reduces pre-storm anxiety and recovery stress. Benefits also include noise reduction, privacy, and slight energy savings from shading.

Final Disclaimer: We are not insurance agents or contractors. This is independent analysis. Your final decision should be made with licensed insurance and construction professionals who can assess your specific property.

🏛️ Authority Insights & Data Sources

▪ Regulatory & Program Framework: Discounts for wind mitigation features are mandated or encouraged by state regulations, such as those outlined by the Florida Department of Financial Services and modeled in programs like Alabama’s FORTIFIED Homes, cited in a February 2026 U.S. GAO report.

▪ Premium & Market Data: 2026 home insurance premium projections and state-level averages are based on analysis from industry sources and Insurify’s market reporting. The link between climate risk, disaster losses, and premium capitalization is supported by academic research inferred from mortgage escrow data.

▪ Industry Trends: The shift towards AI-driven risk scoring, tighter underwriting, and the influence of reinsurance costs on homeowner premiums are documented in 2026 insurance industry analysis.

▪ Note: Insurance discounts, premiums, and program eligibility vary by insurer, state, property, and individual circumstances. This analysis integrates broad market trends and regulatory frameworks; homeowners should confirm specific details with their licensed insurance agent and local building officials.

FAQs: ‘home safety’

Q: How do I actually claim the insurance discount after installing storm shutters?

Q: Do roll-down or accordion shutters give a bigger insurance discount?

Q: My home is not in Florida. Can I still get a discount for storm shutters?

Q: How much does a wind mitigation inspection cost, and is it worth it?

Q: If I get a discount now, can my insurer take it away later?

In the face of rising 2026 premiums, storm shutters are a rare win-win: they enhance safety and trigger verifiable insurance savings. The process is systematic: choose approved products, install correctly, document meticulously, and pass the inspection. Shutters -> Lower Risk -> Better Climate Score -> Discount.

The journey we’ve outlined is based on documented success paths. The common thread is diligence—gathering the right documents, hiring qualified professionals, and using the inspection as an ally. You now have that blueprint. Start by calling your insurer today with the specific question: ‘What is the process and approved product list for a wind mitigation credit for storm shutters?’ That first call sets everything in motion.