The first major financial development this morning: The United States launched Trump Accounts for children on July 4, 2026, giving every eligible child a $1,000 seed deposit invested in the S&P 500. But for Canadian retirees, the story is starkly different—your RRSP must be converted to a RRIF or annuity by December 31 of the year you turn 71. Failure to convert triggers immediate tax on the entire RRSP at your marginal rate, a costly mistake that most Canadians don’t realize. According to a 2025 survey, 57% of Canadians do not know about this mandatory rule.

Today’s Morning Impact Analysis (Top Market Hooks)

- Immediate Action: Check your birth year – if you turn 70 in 2026, you have 18 months to plan your RRSP conversion.

- Hidden Risk: 57% of Canadians are unaware of the mandatory conversion rule – don’t be one of them.

- Money Impact: A missed conversion could cost you 30-50% of your RRSP in one tax year.

RRSP Withdrawal Rules at Age 71: The Core Facts

Mandatory Conversion: What You Must Do by Age 71

By December 31 of the year you turn 71, your RRSP must be converted to a RRIF (Registered Retirement Income Fund) or used to buy an annuity. If you miss this deadline, the Canada Revenue Agency (CRA) treats the entire RRSP as withdrawn in one day, taxing it at your highest marginal rate. This is not a penalty—it is a deemed disposition that destroys years of tax-deferred growth instantly. Visit your financial institution to complete the rrsp withdrawal online conversion form or go in-branch at least one month before your 71st birthday to avoid last-minute errors.

RRSP Withdrawal Rules at Age 71: Minimum Withdrawal Factors

Once converted to a RRIF, you must withdraw a minimum percentage each year, starting at 5.40% at age 71. The CRA prescribes these factors to deplete the RRIF by age 95. Withdrawals are fully taxable as income. Withdrawing more than the minimum is optional but may increase your tax burden.

| Age | Minimum Withdrawal Factor |

|---|---|

| 71 | 5.40% |

| 72 | 5.47% |

| 73 | 5.55% |

| 74 | 5.63% |

| 75 | 5.71% |

| 76 | 5.79% |

| 77 | 5.87% |

| 78 | 5.95% |

| 79 | 6.04% |

| 80 | 6.13% |

For example, with a $200,000 RRIF at age 71, your minimum rrsp withdrawal is $10,800. Use a rrsp withdrawal tax calculator to estimate annual taxable income. The rrsp withdrawal calculator from CRA can help you plan.

Top Tax Mistakes to Avoid During RRSP Withdrawal

Mistake #1: Withdrawing Too Much in One Year

Taking a large lump sum from your RRSP or RRIF can push you into a higher tax bracket. For example, withdrawing $50,000 in one year could cost an extra $12,000 in taxes compared to spreading the withdrawal over two years. Additionally, the OAS clawback threshold for 2026 is $86,912; if your taxable income exceeds that, 15% of the excess is repaid. Tax brackets are indexed annually – timing withdrawals strategically can save thousands. Use an rrsp withdrawal tax calculator to compare scenarios.

Consider the case of Jane, a 72-year-old retiree. She withdrew $50,000 for a home renovation. That lump sum pushed her from the 29% bracket to the 33% bracket, costing an extra $2,000 in federal tax alone. Moreover, her OAS clawback ate another $1,500. If she had spread the withdrawal over two years, she would have saved about $3,500. This is where most people quietly lose money without realizing it.

Mistake #2: Forgetting About Spousal RRSP Rules

If you contributed to a spousal RRSP, withdrawals within three years of the contribution are attributed back to you as income. This can double the tax burden unexpectedly. The attribution rule destroys the tax splitting you were aiming for. Plan spousal RRSP withdrawals at least three full calendar years after the last contribution to avoid attribution. Track the dates carefully in a spreadsheet.

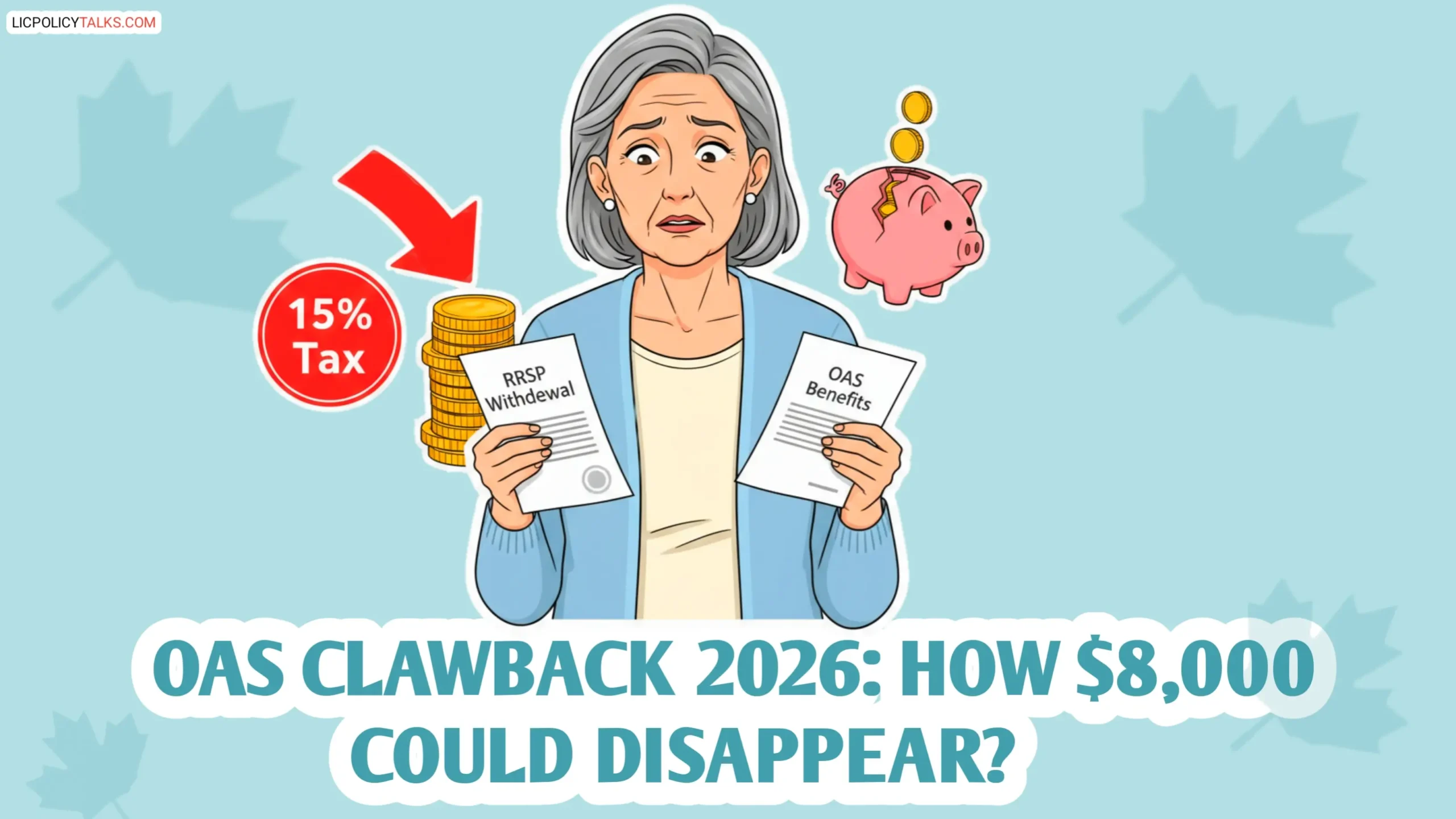

Mistake #3: Ignoring the OAS Clawback Trap

Higher RRSP or RRIF withdrawals increase your income, potentially triggering the OAS clawback. The clawback threshold for 2026 is $86,912; above that, 15% of the excess must be repaid. You could lose up to $8,000 per year in benefits. Many retirees don’t realize OAS is tied to taxable income – RRIF withdrawals count. Use an OAS clawback calculator to plan withdrawals.

| Total Taxable Income | OAS Clawback (Annual) |

|---|---|

| $90,000 | $463 |

| $100,000 | $1,963 |

| $120,000 | $4,963 |

RRSP Withdrawal Tax Calculator and Planning Strategies

How to Use an RRSP Withdrawal Tax Calculator Effectively

An rrsp withdrawal tax calculator helps you estimate taxes before you take the money. For example, if you withdraw $20,000 from your RRSP when your only other income is $30,000, your total income becomes $50,000. The federal tax calculator shows an estimated tax at the 20.5% bracket. This avoids surprise tax bills at filing time. Try the CRA tax calculator or a third-party tool. Remember, each rrsp withdrawal can raise your marginal rate, so always run the calculator with the added income.

Income Splitting and Timing Strategies to Reduce Taxes

Pension income splitting allows you to transfer up to 50% of eligible pension income, including RRIF withdrawals, to your spouse. This lowers the overall household tax bill. Combine with spousal RRSP timing and TFSA withdrawals for maximum efficiency. File Form T1032 to split pension income. However, income splitting does not reduce total tax; it redistributes it. But if your spouse is in a lower bracket, the combined bill drops. Run the numbers before filing.

Federal Reserve Pivot and Its Impact on Your RRSP Investments

How Interest Rate Changes Affect RRSP Growth and Withdrawal Timing

With expectations of a Federal Reserve pivot, bond and equity markets may shift, impacting your RRSP balances. Fed pivot expectations have led to stock market volatility; analysts recommend certain stocks as defensive plays. A larger RRSP balance means higher minimum withdrawals at 71, which could push you into a higher bracket. Consider rebalancing your portfolio to more conservative assets as you approach 71 to reduce sequence-of-returns risk. Review your asset allocation with a licensed advisor.

Expert Task Forces: What Can Canadian Regulators Learn?

Harvard Professors Join Fed Task Forces – Could Canada Follow Suit?

Four Harvard professors and three alumni have joined Fed task forces examining monetary policy. If Canada’s central bank adopts similar reviews, it could influence interest rate decisions and thus RRSP returns. Canadian retirees should monitor both US and Canadian policy shifts as they affect investment income. Set up Google Alerts for ‘Bank of Canada policy review’ and adjust withdrawal plans accordingly.

Frequently Asked Questions About RRSP Withdrawal at 71

FAQs: RRSP Withdrawal at 71

Q: What happens if I don’t convert my RRSP by age 71?

Q: Can I withdraw from my RRSP before 71 without penalty?

Q: How much tax will I pay on an rrsp withdrawal of $10,000?

Q: What is the best strategy to minimize taxes when converting RRSP to RRIF?

Q: Does RRSP withdrawal affect spouse’s benefits?

Authority Insights Box

Expert Take: The Hidden Opportunity in RRSP Conversion

Most advisors focus on the tax hit, but converting early (age 65-70) allows you to use the $2,000 pension income tax credit each year – something you lose if you wait until 71. Conventional wisdom says wait, but that may cost you up to $2,000 per year in missed credits. If you have low-income years between retirement and 71, start phased RRIF withdrawals to use the credit. For example, if you start at 65 instead of 71, you claim the credit for six extra years, saving $12,000 in taxes at a 20% rate.

End Disclaimer / Final Advisory

The information provided is for educational purposes and does not constitute personalized financial advice. Retirement planning involves complex tax rules – consult a certified financial planner or tax professional before making decisions. Market conditions and tax laws are subject to change. Always verify with official sources such as the Canada Revenue Agency. Don’t take this as legal cover – your retirement is unique. If you have over $500k, spending $1,500 on a fee-only planner could save you $50,000 over a decade.

Bottom Line: The next 24 hours are critical – check your birth year and start planning your rrsp withdrawal strategy today. A late decision locks in the loss.