⚠️ User Impact Alerts

- Miss the Dec 31 deadline → Your entire RRSP is deemed withdrawn and taxed as income at your marginal rate. This could mean a $70,000+ tax bill on a $200,000 RRSP.

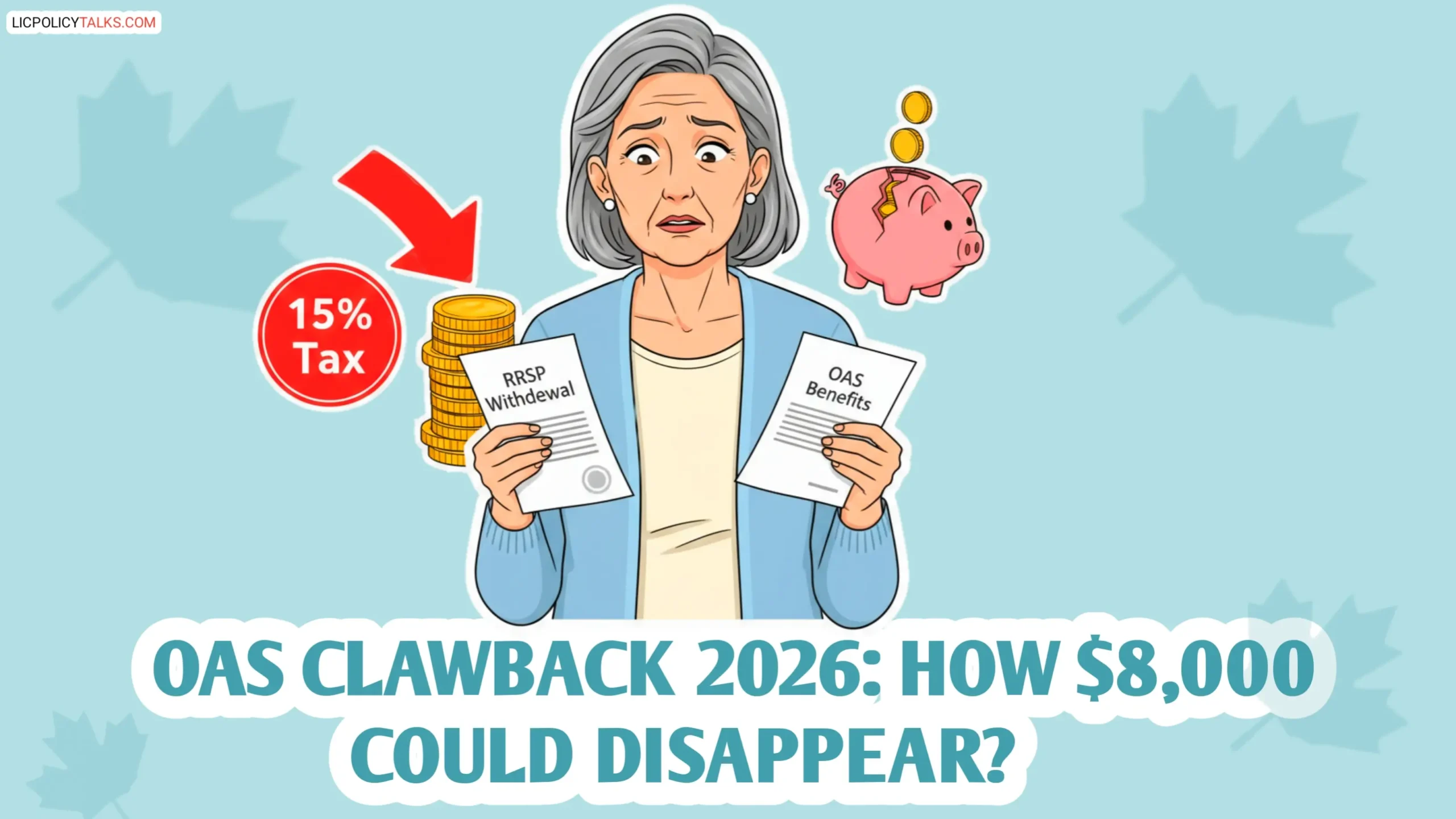

- Withdrawals can trigger OAS clawback. If your income exceeds $79,000 in 2026, you will repay 15% of the excess.

- Use a RRIF to spread tax burden. Minimum withdrawals are lower and you control the tax hit.

- There is no $2,000 tax-free rrsp withdrawal. This myth is false. Every dollar is taxable.

A 2026 Bloomberg retirement survey reveals that fear of outliving money is at a record high. For Canadians approaching age 71, this fear becomes a concrete deadline: convert your RRSP to a Registered Retirement Income Fund (RRIF) by December 31 of the year you turn 71. Failure to do so triggers an immediate deemed withdrawal—and a massive tax bill. Understanding the rrsp withdrawal rules now can save you thousands. In this guide, we break down the exact deadlines, your options (RRIF, annuity, or lump sum), tax implications, and common mistakes. Whether you are turning 71 this year or planning ahead, this is your complete roadmap to avoiding penalties and optimizing your retirement income.

An rrsp withdrawal after age 71 is not optional—it is mandatory by law. Understanding the rules for rrsp withdrawal at this age is critical to avoid taxation at your highest marginal rate.

Why Age 71 Is the Deadline You Can’t Ignore for Your RRSP

According to the 2026 Bloomberg retirement survey, fear of outliving money is at a record high. But for Canadians, the immediate fear should be missing the deadline to convert your RRSP to a Registered Retirement Income Fund (RRIF) by December 31 of the year you turn 71.

The Canada Revenue Agency (CRA) mandates this conversion. If you miss it, the entire RRSP is deemed withdrawn and fully taxed as income. For example, a retiree with a $200,000 RRSP who misses the deadline could face a $70,000+ tax bill, depending on their province and marginal rate. That is a brutal surprise no one wants.

| Birth Year | Conversion Deadline |

|---|---|

| 1955 | December 31, 2026 |

| 1954 | December 31, 2025 |

| 1956 | December 31, 2027 |

Here is the uncomfortable reality: A $250,000 RRSP that is deemed withdrawn in full could push your taxable income to over $250,000 in a single year, resulting in a tax bill of $100,000 or more in Ontario. Most people think they can fix it later, but CRA treats it as an immediate withdrawal with no appeal.

A common mistake is assuming your bank will handle the conversion automatically. Banks notify you but do not execute without your instruction. Log in to your online banking and check the rrsp withdrawal online section for maturity options. A delay of even a few weeks could push the conversion into January, triggering penalties.

The Dec 31 Deadline: What You Must Do Before Year-End

Here is your step-by-step action plan to meet the deadline:

- Contact your bank or brokerage (e.g., RBC, TD Direct Investing).

- Choose between a RRIF, annuity, or lump-sum withdrawal.

- Complete the rrsp withdrawal form online. Use the rrsp withdrawal online portal at your financial institution.

- Submit before December 31 to avoid deemed withdrawal.

If you miss the deadline, CRA deems the entire RRSP as income, taxed at your marginal rate. This could result in a tax bill of $70,000 or more on a $200,000 RRSP. There is no appeal—the deadline is strict.

Your RRSP Withdrawal Options at 71: RRIF, Annuity, or Lump Sum

At age 71, you have three main options for your RRSP:

- RRIF – Minimum withdrawals, tax-deferred growth, flexible income.

- Annuity – Guaranteed income for life, but locked in and dependent on rrsp rates at conversion.

- Lump Sum – Full withdrawal in one year, but taxed entirely at your marginal rate.

Consider a $500,000 RRSP. With a RRIF, minimum withdrawal at age 71 is about 5.28% ($26,400). With an annuity, you might get $25,000–$30,000 per year depending on rrsp rates. With a lump sum, you would pay tax on the entire $500,000, likely at the highest bracket. Understanding your rrsp withdrawal options at age 71 is key.

| Feature | RRIF | Annuity | Lump Sum |

|---|---|---|---|

| Income Flexibility | High – choose minimum or more | Low – fixed payments | One-time |

| Tax Control | Manageable – spread over years | Spread over life | All in one year – highest tax |

| Longevity Risk | You bear risk (market) | Insurer bears risk | N/A |

| Suitability | Most retirees | Those seeking guaranteed income | Only if you need cash and can handle tax |

How to Handle a Spousal RRSP at Age 71

If you have a spousal RRSP, it converts similarly when the annuitant turns 71. Contributions to a spousal RRSP must stop when the contributor turns 71. Review beneficiary designations and consider income splitting. CRA provides spousal RRSP information in both English and French (rrsp in french). Spousal rrsp withdrawal rules also apply.

Bitter truth: Many couples overlook that after turning 71, you can no longer contribute to your spouse’s RRSP. If you overcontribute, you face a 1% monthly tax on the excess. That is $100 per month on a $10,000 overcontribution. Also, ensure your beneficiary is correctly named on the spousal RRSP. If not, your RRSP goes to your estate and is fully taxed.

Tax Implications of RRSP Withdrawals at Age 71

Withdrawals from your RRSP are subject to withholding tax. For example, a $50,000 lump-sum withdrawal in Ontario may face a 20% withholding tax, but in Quebec it could be higher. Withdrawals over $100,000 can push you into a 45%+ marginal rate. Each rrsp withdrawal is subject to withholding tax. Use the rrsp withdrawal tax calculator on the CRA website to estimate your tax bill.

Additionally, RRSP withdrawals count as income for the OAS clawback test. In 2026, if your income exceeds $79,000, you repay 15% of the excess. This can effectively increase your marginal tax rate by 15%. Use the rrsp withdrawal tax calculator to see the impact.

Common RRSP Withdrawal Mistakes at 71 and How to Avoid Them

Many retirees make costly mistakes. Here are the top five:

- Missing the deadline – Already covered, but worth repeating.

- Forgetting to withdraw before conversion if you plan a lump sum – Excess contribution tax applies.

- Overlooking GIS impact – RRSP income reduces Guaranteed Income Supplement benefits.

- Following finfluencer advice – Many younger investors turn to finfluencers for retirement advice, but RRSP rules require professional knowledge. A generic tip could cost you thousands in taxes.

- Believing in the $2,000 tax-free rrsp withdrawal myth – There is no such exemption. It likely came from a misunderstanding of the RRIF minimum.

Myth Busted: There Is No $2,000 Tax-Free RRSP Withdrawal

This myth circulates widely on social media and even some advisor websites. It is completely false. The closest real rule is the $2,000 RRIF minimum withdrawal waiver for those under 65, but that is a calculation, not a free withdrawal. Every dollar withdrawn from an RRSP is fully taxable as ordinary income.

Scenario: Imagine a retiree withdraws $5,000 thinking $2,000 is tax-free. They report $3,000 on their tax return, but CRA sees the full $5,000 as income. They get a reassessment with interest and penalties. That is a $500+ mistake for a $2,000 “benefit” that never existed.

Before believing any “tax-free” claim, use the rrsp withdrawal tax calculator to see the real after-tax amount. CRA’s own French page (rrsp in french) confirms no such exemption exists.

Beyond Age 71: How New Government Programs Affect Your RRSP Strategy

Prime Minister Mark Carney recently unveiled an $18 billion Canadian investment fund on April 27, 2026, aimed at boosting national retirement savings. However, this fund is a separate sovereign wealth fund and does not change your personal RRSP withdrawal rules. You still must convert your RRSP by age 71.

Planning for Cognitive Decline: Why Early RRSP Withdrawal Strategy Matters

Cognitive decline is a growing threat to financial security, as reported by InsuranceNewsNet. Setting up a realistic withdrawal plan early can prevent costly mistakes later. Action step: name a trusted contact person on your CRA account. Use the rrsp withdrawal online feature at your bank to set up automatic RRIF payments.

Tools to Simplify Your RRSP Withdrawal Decision

Essential tools for managing your RRSP conversion:

- CRA My Account – Check your RRSP contribution room and history.

- rrsp withdrawal tax calculator – Use CRA’s official calculator to estimate tax.

- Online banking – Most banks allow rrsp withdrawal online and offer the rrsp withdrawal form.

- CRA French page – Information is available in French (rrsp in french).

- Annuity rate comparisons – Check current rrsp rates offered by insurers.