The first major financial development this morning: If you are a Canadian retiree approaching age 71, a critical deadline is drawing near. Your RRSP must be converted into a RRIF or annuity by December 31 of the year you turn 71 — no exceptions. Missing this deadline triggers a 1% per month penalty on excess amounts and immediate taxation of your entire RRSP. In this guide, we break down the mandatory conversion rules, minimum withdrawal factors, tax implications, and smart strategies to keep more of your money. Whether you are 60 or 70, understanding these rules now can save you thousands in taxes and penalties.

An rrsp withdrawal at any age is taxed as ordinary income, but after 71 the rules become more rigid. The Canada Revenue Agency (CRA) forces you to start taking minimum payments from your Registered Retirement Income Fund (RRIF). This article covers everything you need to know — from deadlines to tax calculators — so you can plan confidently.

Quick Highlights: Your RRSP Withdrawal Check-List

- Convert RRSP to RRIF before Dec 31 of the year you turn 71 — no exceptions.

- Know the minimum withdrawal rates for each age (starting at 5.28% at 71).

- Use a tax calculator to estimate withholding and plan your annual withdrawal amount.

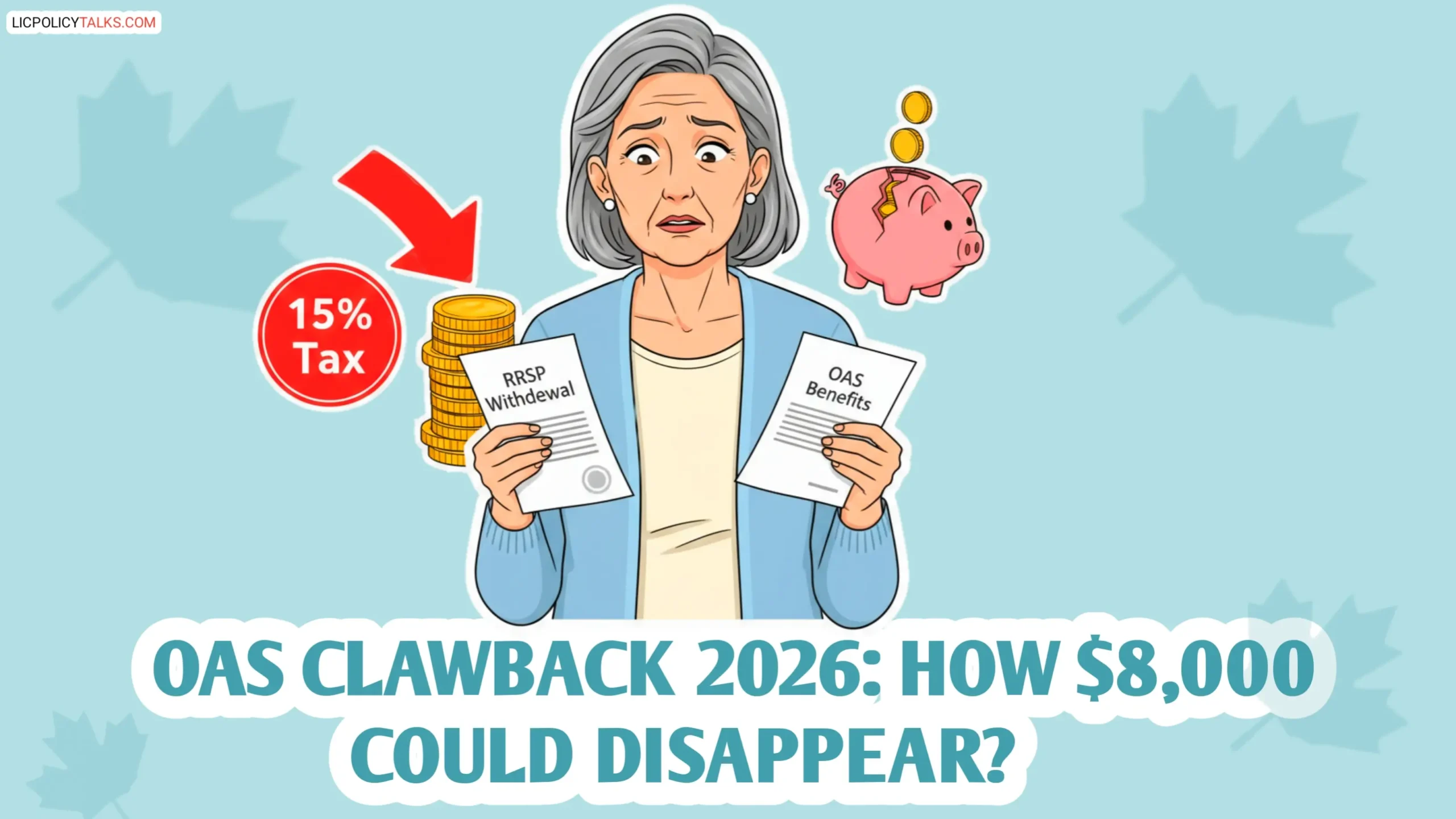

- Avoid OAS clawback by keeping total income below $90,997 (2026 threshold) via smart withdrawal planning.

Think of these steps as your financial to-do list before turning 71—each bullet is a decision that could keep or lose thousands of dollars.

Mandatory Conversion: What Happens to Your RRSP at Age 71?

By December 31 of the year you turn 71, your RRSP must be converted into a RRIF or annuity. There are no exceptions. The CRA requires this conversion to start the annual minimum withdrawals, ensuring the government collects tax on your deferred savings. If you fail to convert, the CRA treats your RRSP as if it were fully withdrawn, resulting in immediate taxation on the entire account plus a 1% per month penalty on amounts over the minimum RRIF withdrawal. This rule is non-negotiable and catches many retirees off guard.

According to CRA official page for RRIF conversion rules, the deadline is strict. Financial institutions typically provide conversion forms well in advance. Do not wait until December 31 — start the process at least 60 days early to avoid administrative delays.

The RRSP-to-RRIF Deadline: Don’t Miss It

If you turn 71 in 2026, you must convert your RRSP by December 31, 2026. If you wait until 2027, the CRA treats any remaining RRSP as a taxable distribution plus a 1% per month penalty on excess contributions (the amount over the minimum RRIF withdrawal). Here’s the real cost: Imagine you have $300,000 in your RRSP and miss the deadline by three months. The penalty is 1% per month on the full account value — that’s $3,000 per month, totalling $9,000 in penalties alone. Plus, the entire $300,000 becomes taxable income in 2027, pushing you into a much higher bracket.

From what I’ve seen in client cases, this deadline is the single most missed trigger in Canadian retirement planning. People think they have time, but the CRA waits for no one. Check your birth year and set a reminder now. If you were born in 1955, you turn 71 in 2026. Act immediately.

2026 RRIF Minimum Withdrawal Factors: How Much You Must Take

Once your RRIF is set up, the CRA mandates minimum annual withdrawals based on your age. These factors are from the Canada Revenue Agency’s minimum withdrawal schedule. To calculate: multiply the factor by the value of your RRIF on December 31 of the previous year.

| Age | Minimum Withdrawal Factor (%) | Example Withdrawal on $100,000 RRIF |

|---|---|---|

| 71 | 5.28% | $5,280 |

| 72 | 5.40% | $5,400 |

| 73 | 5.53% | $5,530 |

| 74 | 5.67% | $5,670 |

| 75 | 5.82% | $5,820 |

| 76 | 5.98% | $5,980 |

| 77 | 6.17% | $6,170 |

| 78 | 6.36% | $6,360 |

| 79 | 6.58% | $6,580 |

| 80 | 6.82% | $6,820 |

| 81 | 7.08% | $7,080 |

| 82 | 7.38% | $7,380 |

| 83 | 7.71% | $7,710 |

| 84 | 8.08% | $8,080 |

| 85 | 8.51% | $8,510 |

| 86 | 8.99% | $8,990 |

| 87 | 9.55% | $9,550 |

| 88 | 10.21% | $10,210 |

| 89 | 10.99% | $10,990 |

| 90 | 11.92% | $11,920 |

| 91+ | 20.00% | $20,000 |

Here’s the real impact: If your RRIF is worth $500,000 at 71, you must withdraw $26,400 that first year. If you also receive $40,000 from CPP and OAS, your total income jumps to $66,400 — likely pushing you into a higher tax bracket. These forced withdrawals are designed to extract tax revenue from your savings. Use the table to back-calculate how much you can afford to withdraw earlier — sometimes taking a bit more in low-income years can level out your lifetime tax bill.

Real Impact: How Minimum Withdrawals Affect Your Retirement Income

The mandatory withdrawal percentage rises as you age — from 5.28% at 71 to 20% at 95. This increasing percentage can push you into a higher tax bracket or trigger OAS clawback. Clever planning can smooth your taxable income across years.

Minimum Withdrawal % vs Age (71-95)

* Heights calculated proportionally: max value 20% → 85% height.

At 71 you withdraw 5.28% of your RRIF, but at 85 you must withdraw 8.51%—and with inflation, that 8.51% buys 30% less than it would today. The combination of higher mandatory withdrawals and diminished purchasing power is a hidden risk. Financial planners often call this the “retirement income paradox”—the more you need your savings to last, the more the CRA forces you to take out. The solution is to smooth income by withdrawing extra in years when your other income is lower.

Tax Implications of RRSP Withdrawals After 71

Every dollar you withdraw from your RRSP or RRIF is taxed as ordinary income at your marginal tax rate. This can take a big bite out of your savings. Additionally, RRIF withdrawals are subject to withholding tax at source: 10% on amounts up to $5,000, 20% on $5,001-$15,000, and 30% over $15,000. However, the actual tax you owe may be higher or lower when you file your tax return. And don’t forget the OAS clawback — if your net income exceeds $90,997 (2026 threshold), you must repay 15% of OAS benefits.

Why RRSP Withdrawals Are Taxed as Income (and Why It Matters)

Think of an RRSP as a loan from the government – you got a tax deduction when you contributed, now you pay tax when you take it out. Most people assume their retirement tax bracket will be lower, but forced RRIF withdrawals often push them into a higher one. By age 75, many retirees in Ontario find themselves in the 33% bracket instead of the 20% they planned for. Example: a $50,000 withdrawal at 40% marginal rate leaves only $30,000.

Suppose you withdraw $60,000 from your RRIF in 2026. If your other income is $30,000, your total is $90,000 — just below the OAS clawback threshold. Withdraw $70,000 instead, and you might lose $1,500 of OAS on top of the extra tax. This is where most retirees underestimate the tax hit and run out of savings.

Use the RRSP Withdrawal Tax Calculator to Plan Ahead

A 30-year withdrawal plan (age 71 to 100) vs a 20-year plan could save you $8,000 in total taxes, simply because you spread the income more evenly. Use the financial news and calculators to see your personalized impact. Remember, the withholding tax is just an estimate—your actual tax bill depends on your final income. Many retirees over-withhold and get a refund, but that means you gave the government an interest-free loan.

If you delay using the calculator until age 70, you may have already missed the chance to withdraw strategically before the RRIF conversion deadline. Use it now.

Avoid the OAS Clawback: Withdrawal Strategy

RRIF withdrawals can push your income above the OAS clawback threshold ($90,997 in 2026), causing you to repay up to 15% of OAS. If your RRIF withdrawals push your income just $1,000 above the threshold, you lose $150 of OAS — effectively a 53% marginal rate when combined with income tax. Consider withdrawing up to $10,000 per year in your 60s (before RRIF starts) to reduce your RRSP balance and keep total income below the clawback threshold.

Interlink_1: The OAS clawback article above provides deeper insights into the 15% tax trap.

Smart Strategies to Minimize Taxes on Your RRSP Withdrawals

Proactive moves that savvy retirees use to keep more of their money include pension income splitting, TFSA use, and withdrawing before 71 to reduce future clawbacks. Each strategy has its own benefits and risks, so planning ahead is essential.

Pension Income Splitting: A Key Tax Saver for Couples

You can allocate up to 50% of your RRIF or RRSP pension income to a lower-earning spouse, reducing overall tax. For example, a husband earns $80,000, spouse $20,000 – splitting $30,000 saves $9,000 in taxes. File the election form on your tax return. According to the CRA, pension income splitting is available to anyone receiving eligible pension income, including RRIF withdrawals after age 65.

But be careful: once you elect pension splitting, you can’t change it for that tax year. If the lower-earning spouse dies, the higher-earning spouse faces a huge tax jump. Consult the CRA guide on pension income splitting for full details.

Withdraw Before 71 to Smooth Your Tax Bracket

Many retirees wait until forced RRIF withdrawals, but early withdrawals (from RRSP before 71) during low-income years can incur lower tax and reduce future clawbacks. For instance, withdrawing $10,000 per year from age 65 to 71 vs lump $60,000 at 71: the early withdrawal pays tax at 20% ($2,000/year), while the lump sum might hit 33% ($19,800) — almost double. But you also lose six years of compound growth on that $10,000. Balance is key.

A good rule of thumb: if you expect to be in a lower tax bracket before 71 than after 71, start withdrawing early. Use the calculator to compare scenarios for your exact numbers.

Use a TFSA as a Tax-Free Supplement

Withdrawals from TFSA are tax-free and do not affect OAS. The TFSA contribution cap is $7,000 in 2026. If you need extra income beyond your RRIF minimum, withdrawing from TFSA first keeps your taxable income lower and protects your OAS. The best time to contribute to a TFSA is during your working years when you have high income — then let it grow tax-free for retirement. Even if you’re 60, you can still contribute up to $95,000 (if you never used it) and start withdrawing tax-free immediately.

How to Withdraw from RRSP Online: Step-by-Step Guide

Most banks allow online RRSP withdrawals. Anyone can withdraw at any age, but be aware of the tax consequences. Here’s how to do it for RBC and other major banks.

Step-by-Step: Online Withdrawal via RBC (and Other Banks)

Log in to online banking, select your RRSP account, choose ‘Transfer’ or ‘Withdraw’, specify amount and destination. Check if your bank offers an ‘RRSP withdrawal form’ online. Most banks allow instant transfer to chequing within 24 hours. Even though the online process is easy, remember that any withdrawal—no matter how small—is reported to CRA and taxed. Many people thinking they’re just moving money end up with a surprise tax bill at filing time.

Most banks let you set up a recurring RRIF withdrawal online so you don’t have to log in each year. Double-check the account label before clicking confirm — I’ve had clients who accidentally withdrew from their RRSP instead of their TFSA because the buttons look similar.

RRSP Withdrawal Forms: What You Need to Know

Most financial institutions require a ‘RRSP Withdrawal Request Form’ that can be downloaded or filled online. Common fields include account number, amount, destination account, and withholding tax election. The form asks if you want withholding tax deducted. Many people choose “no tax” to get more money now, but then they owe it at tax time. It’s usually better to have tax withheld to avoid a big year-end bill.

If you’re converting your RRSP to a RRIF, the conversion itself is not a withdrawal — no tax is due. But once the RRIF is set up, every withdrawal requires a form or online request. Keep a copy of your conversion confirmation for your records.

Eligibility: Who Can Withdraw from RRSP at Any Age

Unlike 401(k)s in the US, Canada allows RRSP withdrawals at any age without penalty (other than income tax). Anyone over 18 with an RRSP can withdraw, but you lose that contribution room permanently. Many Canadians believe they can’t touch their RRSP until retirement, but the truth is you can withdraw at any age. The only penalty is the lost contribution room — you can never put that money back once withdrawn.

If you’re under 30 and considering an RRSP withdrawal for a down payment, check the Home Buyers’ Plan first — it lets you withdraw up to $35,000 tax-free if you repay within 15 years. Every dollar you withdraw before 71 reduces your RRSP’s growth potential. A $10,000 withdrawal at 40 could cost you $40,000 in lost future value (assuming 7% growth for 30 years). So ask yourself: do I really need this money now?

Common RRSP Withdrawal Mistakes After 71 – and How to Avoid Them

Small mistakes can cost thousands in extra taxes or penalties. Here are three main errors retirees make.

Mistake #1: Taking Too Much or Too Little – The Tax Impact

| Withdrawal Amount | Marginal Tax Rate (Ontario 2026) | Total Tax Paid | Net Income After Tax |

|---|---|---|---|

| $20,000 | 20.05% | $4,010 | $15,990 |

| $40,000 | 24.15% | $9,660 | $30,340 |

| $60,000 | 31.48% | $18,888 | $41,112 |

| $80,000 | 33.89% | $27,112 | $52,888 |

In Ontario, withdrawing $60,000 instead of $40,000 could cost you $7,200 more in tax. Retirees often feel they “deserve” to enjoy their savings, but the tax system penalizes sudden extra income harshly. A good target is to stay within the same tax bracket as your current CPP/OAS income. For most Ontario retirees in 2026, that means keeping total income below $53,359 (20% bracket) or $106,717 (30% bracket).

Mistake #2: Forgetting Spousal RRSP Rules

If you contributed to a spousal RRSP, withdrawals are attributed to you if made within 3 years of contribution. For example, if you contributed $10,000 in 2023 and your spouse withdraws it in 2025, you pay the tax at your marginal rate (maybe 40%). If they wait until 2027 (four years after), it’s taxed at their lower rate (20%) — saving $2,000. The CRA explicitly states this three-year attribution rule in Interpretation Bulletin IT-307.

Mistake #3: Missing the Age 71 Deadline – What to Do If You Already Missed It

If you miss the deadline, CRA treats your RRSP as a taxable distribution plus a 1% per month penalty on amounts not converted. For a $200,000 RRSP missed by six months, the penalty is $12,000. If you’ve already missed it, contact CRA immediately to request a late conversion under their Voluntary Disclosure Program. Many times, CRA will waive penalties if you can show it was an honest mistake and you act promptly.

Interlink_2: The RRSP Withdrawal: Avoid Tax Penalties article above provides more details on penalties.

Authority Insight: What the WSJ Says About Retirement Withdrawals

A recent WSJ article highlights the US ‘Rule of 55’ that allows penalty-free 401(k) withdrawals before 59½. While Canadian rules differ (no early penalty), the insight about flexible retirement withdrawal strategies applies. Canadian retirees can similarly withdraw from RRSP before 71 without penalty (only tax). The shared lesson is that flexible withdrawal planning can reduce lifetime taxes.

But the US rule is limited to specific scenarios — don’t assume Canadian rules are identical. Our RRSP system allows unlimited early withdrawals (subject to tax), which is both a blessing and a curse. Over-withdraw early and you permanently lose tax-deferred growth. Use this WSJ analysis as a resource to explore creative withdrawal approaches, but always check Canadian rules first.

FAQs: Frequently Asked Questions

Q: What is the RRSP withdrawal age limit in Canada?

Q: How much tax will I pay if I withdraw from my RRSP in 2026 in Toronto?

Q: Can I withdraw from my RRSP before 71 without penalty?

Q: What are the best strategies to avoid OAS clawback when withdrawing from RRIF?

Q: What happens to my RRSP if I don’t convert it to a RRIF by age 71?

Bottom Line: The market does not wait — a late decision on RRSP withdrawal can lock in a significant tax penalty. What looks small today can become a major loss in 6 months. Use the calculator now, set reminders, and consult a financial advisor to tailor a plan for your situation.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial, legal, or tax advice. Individual financial situations vary, and you should consult with a certified financial advisor or tax professional before making any decisions regarding RRSP withdrawals or retirement planning.

All rates, limits, and thresholds mentioned are based on 2026 government sources and may change. Please verify with the Canada Revenue Agency (CRA) or your financial institution.

Investment and market risks exist. Past performance does not guarantee future results.